Page 19 - CII Artha Magazine 1

P. 19

Global Trends

The monthly trends also show B. LAGGARDS Faster-than-expected OVID-19 is far from

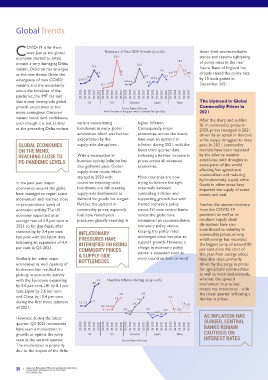

that public spending is normalisation of the US C over. Just as the global Trajectory of Real GDP Growth (y-o-y%) down their accommodative Key Policy Rates (%)

progressing at a rapid clip. As Consumption demand monetary stimulus economy started to settle 23.6 stance and resume tightening 5.0

per the latest data available on continues to move at 18.3 of policy rates in the near 4.3

CGA, capital spending for snail’s pace During the COVID-19 around a very damaging Delta 12.2 14.2 future. Bank of England has 4.0 3.9

April-November FY22 stood pandemic, the US Federal variant, Omicron has emerged 4.9 6.6 7.6 4.9 6.5 7.9 already raised the policy rate 3.0

at Rs 2.73 lakh crore, which is The disaggregated picture Reserve brought short-term as the new threat. Given the 0.5 3.7 1.4 4.9 2.3

13.5 per cent higher in from the demand side shows interest rates to near-zero emergence of new COVID -2.9 -2.3 -5.8 -4.0 -4.4 -1.2 -5.5 -0.9 -1.3 by 15 basis points in 2.0

year-on-year terms and that private final consumption and restarted large-scale variants and the uncertainty -8.1 -7.1 December 2021.

represents 49.4 per cent of expenditure (PFCE) continues bond purchases, referred to about the timelines of the 1.0 0.8

the budgeted spend for the to move at snail’s pace and as Quantitative Easing (QE). It pandemic, the IMF has said Q3 2020 Q4 2020 Q1 2020 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 0.3

current fiscal. Notably, it is 28.0 trails pre-pandemic levels. It helped in sharply bringing that it may downgrade global US UK Eurozone Japan China The Uptrend in Global 0.0 0.1 0.0 -0.1

per cent higher than the same grew at a slower rate of 8.6 down the borrowing costs, growth projections as the Commodity Prices in US UK Eurozone Japan China

Source: National Sources

period in the pre-pandemic per cent in the Q2FY22 as which cushioned the more contagious Omicron Note: The years in the graph refer to Calendar Year (Jan-Dec) 2021 -1.0

year of 2019-20. While the compared to 19.3 per cent in economic recovery process variant could dent confidence, Q3 2019 Q3 2020 Q3 2021

progress so far has been good, the previous quarter as in the US. higher inflation. After the sharp and sudden Source: National Sources

to achieve the budgeted capital impact of a favourable base even though it is not as fatal variant necessitating fall in commodity prices in

expenditure of Rs 5.5 lakh effect waned. With this, the However, in his recent as the preceding Delta variant. lockdowns in many global Consequently, major 2020, prices resurged in 2021

economies, across the board,

economies which was further

TAKING STOCK heartening to note that the A. DRIVERS OF GROWTH crore, the capex push by the Sectors such as Transport In absolute terms, the consumption spending grew remarks, the Federal Reserve exacerbated by the have seen an uptrend in driven by an uptick in demand Moving ahead, trade (exports and as per the World Trade

while supply struggled to keep

government needs to be

by 13.5 per cent in the first

Organization (WTO) global

and imports) registered a

merchandise exports have

services, Construction &

Chair Jerome Powell has

real GDP in absolute terms at

inflation during 2021, with the

supply-side disruptions.

OF THE YEAR Rs 35.7 lakh crore in the Public investment sustained. One of the ways to Real Estate, Metals & Metals reached a cumulative value half of the current fiscal. indicated that the Fed will GLOBAL ECONOMIES latest third quarter data pace. In 2021, commodity sharp recovery in 2021 trade volumes are expected

markets have been impacted

ON THE MEND;

do so is to expedite the

However, encouragingly,

Products and Chemicals &

of US$299.7 billion between

backed by the resumption in

to rise by 10.8 per cent in

continues to do the

start tapering its bond

second quarter of this fiscal

has crossed the pre-pandemic heavy lifting as the key projects delineated under the Chemical Products, where April-December 2021, private consumption is now purchases soon in order to REACHING CLOSE TO With a resumption in indicating a further increase in by the adverse weather business activity and strong 2021, followed by a 4.7 per

conditions, with droughts in

National Infrastructure

at 96 per cent of the

prices across all advanced

business activity, inflation has

sustained demand recovery is

The GDP print during levels of Rs 35.6 lakh crore demand-side driver of Pipeline (NIP), which are visible, are driving the recovery in which amounts to 75 per pre-pandemic level. keep inflation in check. This is PE-PANDEMIC LEVELS also gathered pace. Global economies. some parts of the world demand from businesses and cent increase in 2022.

the economy

Q1FY22 showed that the seen in the second quarter of nearing completion. private investment and account cent of the US$400 billion likely to have repercussions on supply chain issues, which affecting few agricultural

economy expanded by an 2019-20. An analysis of the second for nearly 62 per cent of total export target set up by the Supply-chain bottlenecks interest rates globally, thus started in 2020 with Many countries are now commodities and reducing Overall, key global economies

government.

impressive 20.1 per cent - quarter of this fiscal shows Encouragingly, capital spending private investment spending by stifling growth impulses affecting foreign inflows to hydroelectricity supply while INTERNATIONAL are poised for a recovery in

testifying that the green From supply-side basis, real that public investment has by the government across key end of third quarter. Industrial sectors such as emerging economies like India. In the past year, major countries imposing strict trying to balance the tight floods in other areas have TRADE RECOUPS ON 2021 and while the upward

shoots of economic recovery gross value added (GVA) continued to do the heavy infrastructure sectors has engineering goods, Supply-side bottlenecks However, compared to 2013, economies around the globe lockdowns, are still creating rope walk between impacted the supply of some RECOVERY IN momentum is likely to

are slowly but surely stood at 8.5 per cent in lifting as it bounced back to remained healthy at Rs 1.81 Healthy exports also petroleum products and especially related to coal and the Fed is being more cautious have managed to regain some supply-side bottlenecks as controlling inflation and metals and coal. ECONOMIC ACTIVITY continue in the next year as

becoming visible. However, Q2FY22 as compared to 18.8 the pre-pandemic levels in lakh crore in the period remain an enabler for organic & inorganic global shortage of in normalisation this time, momentum and reached close demand for goods has surged. supporting growth, but with well, we may see a

growth for the second quarter per cent in the previous Q2FY22. Gross fixed capital April-November FY22 which growth in the current fiscal chemicals have driven the semiconductors in the prioritising economic recovery to pre-pandemic levels of Further, the uptrend in limited monetary policy Further, the uneven recovery AND STRONG DEMAND moderation in the growth

of the current fiscal (Q2FY22) quarter. formation (GFCF) was up translates into a healthy 61.7 bulk of the rise in export automobile sector affected even as inflation remains above economic activity. The US commodity prices, especially armor. Till now, central banks from the COVID-19 rates. With regard to inflation,

moderated to 8.4 per cent, 11.0 per cent in the second per cent growth in Global recovery, helped by growth in this fiscal so far. the growth of the industrial the target. The impact of Fed economy expanded at an fuel, have raised price across the globe have pandemic as well as its as demand recovers further,

which is primarily attributed Having taken stock of the quarter, largely supported by year-on-year terms over the rapid pace of vaccination, has Encouragingly, the sector, especially the MSMEs. taper will not be akin to the average rate of 5.9 per cent in pressures globally resulting in maintained an accommodative resultant supply chain households alike. Globally, all cost-push inflation is likely to

central spending, taking

to waning of a favourable base economy, we now bucket the growth to 28.3 per cent in comparable period last year. boosted India’s external labour-intensive sector like This got mirrored in the 2013 taper tantrum episode, 2021 so far (Jan-Sept), after monetary policy stance, disruptions have also major economies reported an firm up resulting in

of last year. movers and shakers of growth the first half of the current demand. Consequently, exports gems & jewellery has also passenger vehicle sales given India’s strong external contracting by 3.4 per cent keeping the policy rates contributed to volatility in uptrend in trade in 2021, inflationary pressures

into the two broad heads of Out of the key infra sectors, have emerged as a critical declining in double digits by fundamentals, especially on the INFLATIONARY commodity prices, among despite supply-side gathering momentum. This is

DRIVERS and LAGGARDS fiscal as compared to 8.6 per Shipping, Road Transport & driver of growth in the current seen robust growth during 18.6 per cent for the third external front. last year, with the latest data PRESSURES HAVE unchanged since last year to which energy has recorded constraints such as port expected to nudge the major

Notwithstanding, the and analyse their performance cent in the similar period in this period. indicating an expansion of 4.9 support growth. However, a

deceleration in growth noted below: 2019-20. Highways, Housing & Urban fiscal. straight month in November per cent in Q3 2021. INTENSIFIED ON RISING change in monetary policy the biggest jump of around 80 backlogs and semi-conductor central banks across the

in the second quarter, it is Affairs and Railways have so far 2021 despite strong demand High global commodity COMMODITY PRICES stance is expected soon as per cent since the start of shortages. world to reverse their

seen higher cumulative in the local market. This was prices pressurise & SUPPLY-SIDE this year. Non-energy prices accommodative monetary

spending during the year as the lowest sales in seven corporate margins Similarly, for other major BOTTLENECKS many countries look to wind have also risen, primarily Global merchandize trade stance and tighten policy

compared to last year. years for passenger vehicles. economies as well, opening of driven by the surge in prices touched its pre-pandemic rates in the coming months.

Global commodity prices businesses has resulted in a for agricultural commodities peak in the first half of 2021

There are many factors have inched higher in the pick-up in economic activity as well as metal and minerals,

Private capex, too, has attributable for the grave current year driven by an with the Eurozone expanding whereas the upward

started showing signs of semiconductor shortages uptick in demand while supply 4.8 5.3 Headline Inflation Inching up (y-o-y%) momentum in precious Trajectory of the Trade Momentum (US$ billion)

recovery as per CMIE’s being felt currently worldwide. has struggled to keep pace. In by 5.6 per cent, UK by 8.1 per metals has moderated - with 4000 500

capex data From the supply side, there 2021, commodity markets cent, Japan by 2.6 per cent 2.8 2.9 the latest quarter indicating a 3000 400

are factors such as temporary have been impacted by and China by 10.4 per cent 2.0 1.8 2.3 decline in prices.

As per CMIE’s capex data, factory closures due to the during the first three quarters 1.2 1.2 1.9 1.0 1.1 0.8 300

private capital expenditure pandemic and disruptions in adverse weather conditions, of 2021. 0.6 0.5 0.6 0.0 0.0 0.1 0.0 2000 200

(measured by the value of supply as storms halted with droughts in some parts -0.3 -0.9 -0.5 -0.7 -0.2

ongoing projects) stood at Rs production facilities in the US of the world affecting a few However, during the latest AS INFLATION HAS 1000 100

71.7 lakh crore at the end of and Japan. The demand-side agricultural commodities and quarter, Q3 2021, economies SURGED, CENTRAL 0 0

third quarter- higher than the factors include huge backlog reducing hydroelectricity have seen a moderation in Q3 2020 Q4 2020 Q1 2020 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 BANKS REMAIN Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q3 2020 Q4 2020 Q1 2021

Rs 69.27 lakh crore print seen of demand for chips due to supply while floods in other growth, as against the jump US UK Eurozone Japan China CAUTIOUS ON

in the same period in FY21 and the release of pent-up demand areas has impacted the supply seen in the second quarter. INTEREST RATES US UK (RHS) European Union Japan (RHS) China

Rs 69.39 lakh crore seen in the amongst others. of certain metals and coal. Source: National Sources Source: National Sources & WTO

pre-pandemic period of FY20. The moderation is primarily

due to the impact of the delta

19 ANALYSIS, RESEARCH, THOUGHT LEADERSHIP & ADVOCACY ANALYSIS, RESEARCH, THOUGHT LEADERSHIP & ADVOCACY 20

QUARTERLY JOURNAL OF ECONOMICS

QUARTERLY JOURNAL OF ECONOMICS

DECEMBER 2021 DECEMBER 2021

B. Deepening the supported CAS (conditional

Component Value Chain access system) for set top

across the entire boxes.

ecosystem

Similarly, a global innovation

The domestic electronics challenge for designing of

industry is characterised by semiconductors and chip sets

lack of a component for educational tablets for the

ecosystem which leads to its masses could be encouraged.

dependence on imports. High

dependency on imported Besides, the next focus should

inputs raises cost and impedes be on maximizing domestic

competitiveness. A right mix value addition and promoting

of policy realignment coupled Design in India, besides Make

with new targets is required. in India. For this, the

know-how available with

The government has, no doubt Government owned R&D

announced the PLI scheme for laboratories should be made

components. However, the 5-6 freely accessible to industry,

per cent incentive on outsourced R&D needs to be

incremental sales, envisaged incentivized on the lines of

under the scheme, is not In-house R&D, Technology

enough to achieve scale in this Acquisition Fund be created

sector and accordingly would for liberal assistance in filing

discourage manufacturers patents and a Guarantee Fund

from indigenizing production. be created to help R&D

Hence, the government should houses to raise working

review the scheme by capital.

expanding the incentive from

the present 5-6 per cent and D. Other Suggestions

widen the eligibility criteria. A

revamped PLI would facilitate Similarly, the government

scale economies from should also look at other

domestic production and also options such as leveraging

encourage SMEs to strengthen upcoming FTAs (UK & the

the supply chain and reduce EU) towards enhancing

our dependence on imports. exports, incentivizing

manufacture of products not

C. Encouraging Design-led currently produced in India,

Manufacturing facilitating EoDB, among

others.

For ensuring that the industry

remains competitive (by To conclude, a robust policy

facilitating domestic IP environment would help the

creation), even after the PLI & country to realise the huge

other benefits expire, a push opportunity awaiting India to

to R&D is most essential. For emerge as a global hub for

this, the government should electronics and meet the

explore innovative solutions targets envisioned in the NPE

for the sector such as a model 2019.

based on the Government led

domestic manufacturers